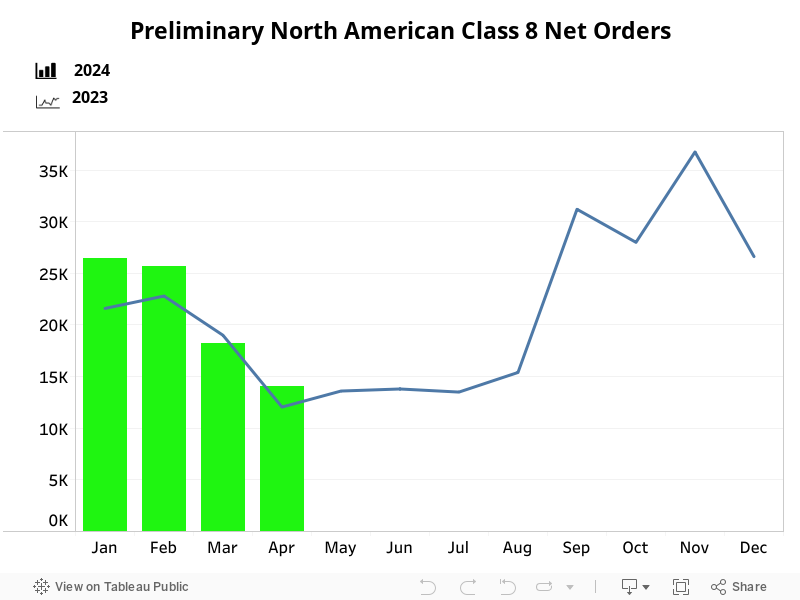

Preliminary North American Class 8 Net Orders Totaled 8,900 Units in June

Preliminary net orders for North American (N.A.) Class 8 trucks/tractors in June totaled 8,900 units, marking declines of 25% month-over-month (m/m) and 36% year-over-year (y/y). Although June typically experiences a modest m/m increase, ongoing tariff volatility coupled with economic and freight market uncertainty led many fleets to scale back their orders. Net orders were significantly below the 10-year average of 19,213 units for June and were the lowest for a June since 2009. Both on-highway and vocational segments experienced reduced demand compared to the previous month, though the on-highway segment accounted for most of the decline. For the 2025 order season so far (September 2024 through June 2025), net orders are down 15%. Class 8 orders for the past 12 months total 255,265.

Ongoing tariff volatility and economic/freight uncertainty continue to disrupt the N.A. Class 8 truck/tractor market as illustrated by the significant 32% y/y decline in net orders during 2025 to date. Recent tariff hikes – most notably the increase from 25% to 50% on steel, aluminum, and fabricated components that took effect June 4 – have significantly raised production costs as demand has deteriorated. Other tariffs are still in flux. The U.S. announced a trade deal with Vietnam just today, but imports from other countries continue to incur a baseline 10% tariff – more for China and certain imports from Mexico and China – pending negotiations.