U.S. Trailer Net Orders for February Reached Nearly 20,900 Units

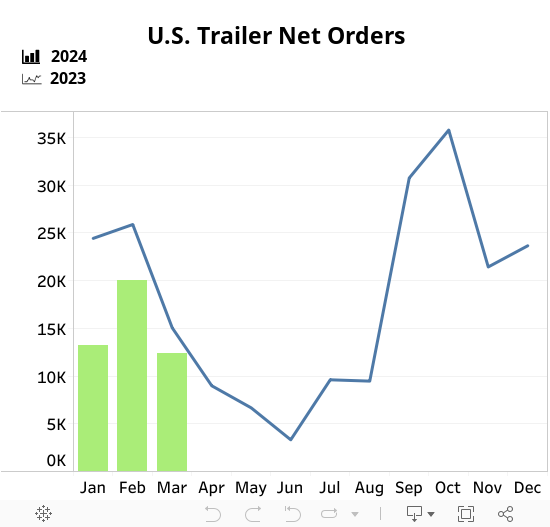

Total U.S. trailer net orders in February declined 18% month-over-month (m/m) but increased 3% year-over-year (y/y), reaching 20,874 units. February represented the fourth consecutive month with net orders exceeding 20,000 units and positive y/y growth. However, a sluggish start to the 2025 order season (September 2024 through February 2025) means that cumulative net orders are still down 14% y/y at 124,737 units. Although many fleets prioritized purchasing power units over trailers in 2024, U.S. trailer net orders of 46,298 for 2025 to date have outpaced U.S. Class 8 net orders by 9,554 units. Whether this trend will continue in the near term is uncertain.

Total trailers built in February increased 23% m/m to 15,800 units but remained down 34% y/y. The stronger-than-seasonal m/m increase was likely driven by improved order levels in recent months and efforts by some OEMs to produce additional units ahead of potential tariffs expected in March or April. Trailer build for 2025 to date is down 34% y/y. With total trailer net orders outpacing production, backlogs increased by 4,298 units, or 4%, m/m. The sharper increase in production than in backlogs reduced the backlog/build ratio slightly to a still-healthy 7.8 months.